How to Estimate Your Social Security Benefits in 2026: Timing, Strategy, and What You'll Actually Receive

If you have a $1 million or more saved in a 401(k) or Individual Retirement Account (IRA), Social Security probably isn't going to be your only source of retirement income. But it's still one of the most important financial decisions you'll make, and one of the most commonly mishandled ones.

The question most people ask is "how much will I get?" But the more important question is "when should I claim, and how does that interact with everything else I have going on?" The answer can be worth hundreds of thousands of dollars over your lifetime.

This guide covers:

How Social Security benefits are calculated

How to get your own personalized estimate in minutes

The breakeven analysis for claiming at 62, 67, or 70

Spousal benefit strategies for married couples

The tax implications of claiming too early (the "tax torpedo")

The 2026 earnings test rules if you plan to keep working

How to use our Social Security Lifetime Benefit Calculator to run your own numbers

Let's start with the basics, then get into the strategy.

What Is Social Security and How Is It Funded?

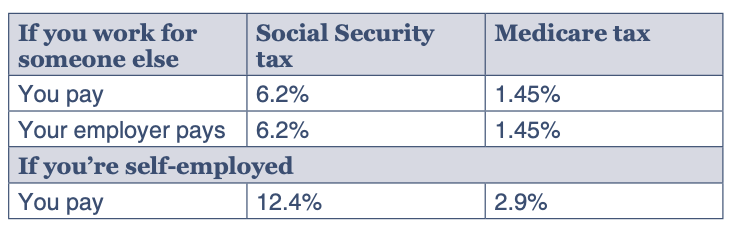

Social Security is a federal program established in 1935 that provides income to retired workers, disabled individuals, and the surviving dependents of deceased workers. It's funded through payroll taxes, specifically the Federal Insurance Contributions Act (FICA) tax, which is split between employees and employers.

Payroll Taxes (or FICA, the Federal Insurance Contributions Act) are deducted from each paycheck.

In 2026, you pay Social Security tax on your first $184,500 of earned income (this wage base adjusts annually for inflation). You pay Medicare tax on all earnings with no cap.

For employees, the combined FICA rate is 7.65% (6.2% for Social Security, 1.45% for Medicare). Your employer matches that amount. If you're self-employed, you pay both sides (15.3% total), though you can deduct half of it on your tax return.

Who Qualifies for Social Security Retirement Benefits?

To qualify for Social Security retirement benefits, you need 40 work credits, which generally means about 10 years of working and paying into the system. In 2026, you earn one credit for each $1,890 of earnings, up to a maximum of four credits per year.

Beyond retirement benefits, Social Security also pays benefits to:

Spouses and dependent children of someone receiving benefits

Divorced spouses (if the marriage lasted at least 10 years)

Surviving spouses and children of deceased workers

Dependent parents of deceased workers

Workers with qualifying disabilities

How Social Security Benefits Are Calculated

Your benefit is based on two things: your Average Indexed Monthly Earnings (AIME) and your Primary Insurance Amount (PIA).

The Social Security Administration (SSA) takes your highest 35 years of inflation-adjusted earnings, adds them up, and divides by the number of months in those years to get your AIME. If you worked fewer than 35 years, the missing years count as zero, which pulls your average down and reduces your benefit.

Your PIA is what you'd receive if you claimed at your Full Retirement Age (FRA). The SSA applies a formula to your AIME that's designed to replace a higher percentage of income for lower earners and a lower percentage for higher earners.

For most people reading this, your Full Retirement Age is 67 (anyone born in 1960 or later). This is the baseline from which early and delayed claiming penalties and credits are calculated.

How to Get Your Personal Benefit Estimate

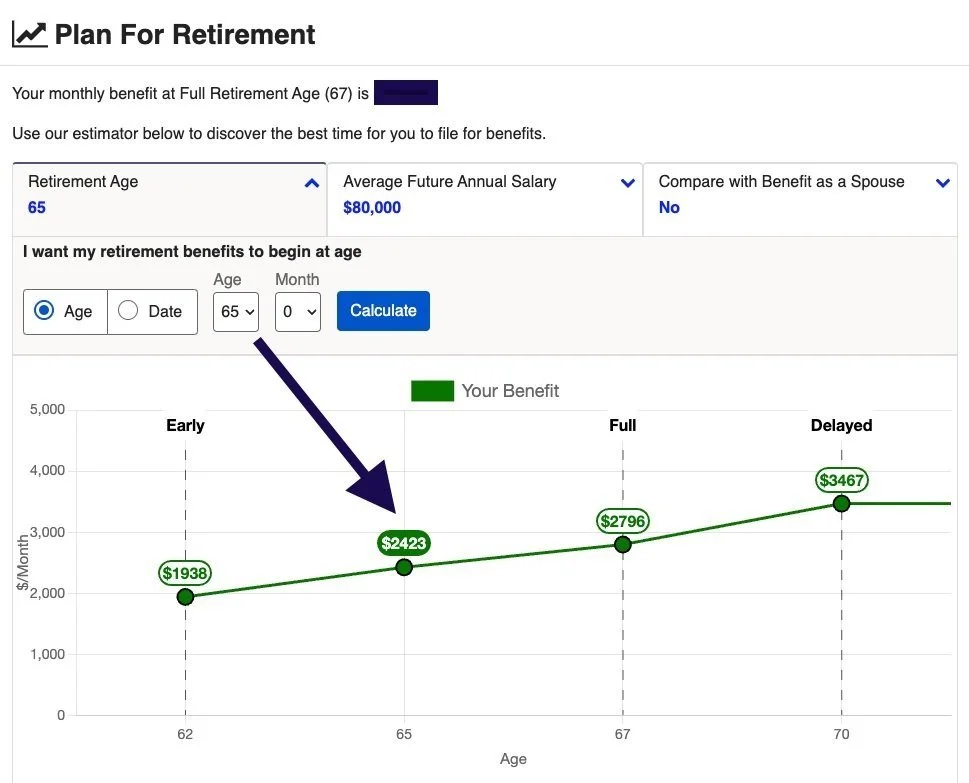

The fastest way to see your own numbers is through your my Social Security account at ssa.gov/myaccount.

Here's how to use it:

Create or log into your my Social Security account at ssa.gov/myaccount

Scroll to the "Plan For Retirement" section after signing in

You'll see estimated monthly benefits automatically displayed at age 62, your full retirement age, and age 70

Use the "Retirement Age" dropdown to see estimates for any claiming age

You can also adjust your projected future earnings to see how working longer (or stopping early) affects your benefit

Retirement Estimator in my Social Security

The estimates assume you'll keep earning at your current rate until you claim. If you plan to retire early or reduce your income before claiming, the actual benefit may be lower than what the tool shows.

The Claiming Age Decision: 62, 67, or 70?

This is the decision that matters most. Claiming age has a permanent effect on your monthly benefit for the rest of your life.

Claiming at 62 (earliest possible): Your benefit is reduced by approximately 30% compared to your full retirement age amount. If your FRA benefit would be $2,800/month, claiming at 62 gives you roughly $1,960/month instead. This reduction is permanent.

Claiming at 67 (Full Retirement Age): You receive your full PIA with no reductions or increases.

Claiming at 70 (maximum delay): Benefits increase by 8% for each year you delay past your FRA, up to age 70. That means a four-year delay from 67 to 70 results in a benefit that's 32% higher than your FRA amount. If your FRA benefit is $2,800/month, claiming at 70 gives you approximately $3,696/month instead.

After age 70, there is no additional increase for waiting longer.

The Breakeven Analysis: When Does Delaying Actually Pay Off?

Delaying to 70 means a bigger monthly check, but you collect fewer checks before you die. So the question is: how long do you need to live for the delay to pay off?

Example: Suppose your FRA benefit at age 67 is $2,800/month and your benefit at 70 is $3,696/month.

Claiming at 67: You collect $2,800/month starting at 67

Claiming at 70: You collect $3,696/month starting at 70, but nothing for 3 years

The 3-year gap means you forgo $100,800 in benefits ($2,800 x 36 months) by waiting.

To calculate the breakeven point, divide the foregone benefits by the monthly difference:

$100,800 / $896 (the monthly difference) = approximately 112 months, or age 79

If you live past age 79, delaying to 70 pays off. If you don't, claiming earlier would have been better in dollar terms.

For a married couple, the math gets more interesting. The higher earner delaying to 70 also increases the survivor benefit. If the higher earner dies first, the surviving spouse receives the larger delayed benefit for the rest of their life. This often makes delaying even more valuable for couples than the simple breakeven math suggests.

Use Our Social Security Lifetime Benefit Calculator

To see how your own numbers play out, use our Social Security Lifetime Benefit Calculator below.

Enter your estimated monthly benefit, a Cost of Living Adjustment (COLA) rate (the average since 1976 has been 3.7%), and the number of years you expect to collect benefits. The calculator will show you your estimated lifetime benefit total and final monthly check after inflation adjustments.

Try running it at three different benefit amounts (your age 62 estimate, your FRA estimate, and your age 70 estimate) to see the lifetime dollar difference across different claiming ages and life expectancies. It's one of the most eye-opening exercises for anyone within 10 years of retirement.

Spousal Benefit Strategy for Married Couples

If you're married, Social Security planning gets more complex, and more valuable when done right.

The spousal benefit basics: A spouse who earned little or no income can claim up to 50% of the higher earner's FRA benefit, even if they never worked. The spousal benefit does not increase beyond 50% if the higher earner delays past FRA, so there's no benefit to the lower earner waiting past their own FRA to claim the spousal benefit.

The survivor benefit: When one spouse dies, the surviving spouse receives the higher of their own benefit or the deceased spouse's benefit. This is why the higher earner's claiming decision matters so much for couples. Delaying to 70 can significantly increase the income the surviving spouse receives for potentially decades.

A common strategy for couples: The lower earner claims early (at 62 or FRA) to bring in some income while the household waits. The higher earner delays as long as possible, ideally to 70, to maximize both their own benefit and the eventual survivor benefit.

There's no one-size-fits-all answer. It depends on both spouses' health, income needs, other assets, and the age gap between them. But running the numbers before claiming is essential.

The Tax Torpedo: Why Claiming Early Can Cost You More Than You Think

Here's something most people don't consider: if you have significant 401(k) or IRA balances and claim Social Security early, you may be creating a tax problem that quietly eats away at your benefits.

The issue is that Social Security benefits become taxable once your provisional income (your Adjusted Gross Income (AGI) + tax-exempt interest + 50% of your Social Security benefits) exceeds certain thresholds. Up to 85% of your Social Security can be subject to federal income tax.

If you claim Social Security at 62 and also need to take 401(k) withdrawals to cover expenses, those withdrawals increase your provisional income and can push a large portion of your SS benefit into taxable territory. This effectively reduces the net value of claiming early.

On the other hand, if you delay Social Security and spend down your traditional IRA or 401(k) first, or do strategic Roth conversions during those years, you may be able to control your income in a way that reduces lifetime taxes significantly.

This is one of the most overlooked intersections in retirement planning. For a deeper look at how retirement income is taxed, including the full provisional income calculation, see our guide to how retirement income is taxed in 2026.

The 2026 Earnings Test: What Happens If You Keep Working

If you claim Social Security before your Full Retirement Age and continue to earn income from work, the earnings test applies.

In 2026, the SSA reduces your benefit by $1 for every $2 you earn above $24,480 per year ($2,040 per month). In the calendar year you reach your FRA, a more lenient test applies: $1 reduced for every $3 earned above $65,160 ($5,430 per month).

Once you reach your Full Retirement Age, the earnings test disappears entirely. You can earn any amount with no reduction to your benefit.

Important clarification: the withheld benefits aren't permanently lost. Once you reach FRA, the SSA recalculates your benefit upward to account for the months where payments were withheld. But it still affects your cash flow in the short term and the breakeven math changes if you're working and claiming simultaneously.

Strategies to Maximize Your Social Security Benefits

1. Work at least 35 years. Your benefit is based on your highest 35 years of earnings. Every zero year in the calculation drags your benefit down. Working a few extra years to replace low-earning years with higher-earning ones can meaningfully increase your benefit.

2. Check your earnings record for errors. Log into your my Social Security account and review your annual earnings history. Mistakes happen, and an error from 20 years ago that went uncorrected could be quietly reducing your benefit. You can request corrections through the SSA.

3. Understand the delayed credits. The 8% annual increase from 67 to 70 is guaranteed and risk-free. No investment reliably delivers 8% annually with zero market risk. For people in good health with longevity in their family, this is often the most valuable "investment" available to pre-retirees.

4. Coordinate with your spouse. As described above, the claiming sequence between spouses matters, especially the higher earner's decision, which affects the survivor benefit.

5. Factor in taxes before you decide. Your net benefit after taxes is what matters, not the gross monthly check. Running the numbers with a financial planner before you claim can reveal strategies that save tens of thousands in lifetime taxes.

Frequently Asked Questions

At what age can I start collecting Social Security? You can begin collecting as early as age 62, but your benefit will be permanently reduced. Full benefits are available at your Full Retirement Age (67 for anyone born in 1960 or later). Delaying past FRA increases your benefit by 8% per year up to age 70.

What happens to my Social Security if I claim early and then go back to work? If you're under your FRA and earning above the earnings test threshold ($24,480 in 2026), the SSA will withhold $1 for every $2 you earn above that limit. Once you reach FRA, your benefit is recalculated upward to account for withheld months, but it can create cash flow complications in the meantime.

Can my spouse receive Social Security benefits based on my record? Yes. A spouse can receive up to 50% of your FRA benefit, even with little or no work history of their own. The spouse must be at least 62, and you must already be receiving your own benefit for them to claim the spousal benefit.

Does delaying Social Security affect my Medicare enrollment? Not directly, but it's important to know that Medicare eligibility begins at age 65 regardless of when you claim Social Security. If you're not yet receiving Social Security at 65, you need to actively enroll in Medicare Part B during your Initial Enrollment Period or you may face a permanent premium penalty.

Is Social Security going broke? The Social Security trust funds face a long-term funding gap. Current projections from the SSA suggest that if no changes are made, the trust funds could be depleted around 2033-2035, at which point incoming payroll taxes would cover approximately 75-80% of scheduled benefits. Most experts expect some combination of benefit adjustments and tax changes before any cuts take effect, but it's a legitimate factor to consider in planning, especially for younger pre-retirees.

How does Social Security factor into my overall retirement tax strategy? Significantly. The timing of your Social Security claim interacts with your 401(k) withdrawals, Roth conversions, and Medicare premiums in ways that can either cost you or save you a substantial amount over retirement. See our full guide on how retirement income is taxed in 2026 for the details.

In Closing

Estimating your Social Security benefit is straightforward. Deciding when to claim, and how to coordinate that decision with your taxes, your spouse's benefit, your 401(k) withdrawals, and your Medicare enrollment, is where the real planning happens.

For most people with $1 million or more in pre-tax retirement accounts, Social Security timing is one piece of a larger puzzle. Getting it right can add tens of thousands of dollars in lifetime income and significantly reduce your lifetime tax bill.

If you'd like help thinking through your Social Security strategy as part of a complete retirement plan, we'd be glad to walk through it with you.

To your Atomic Retirement,

Ryan Kilkenny

P.S. If you have a question or would like help with your Social Security strategy, you can schedule an appointment here.

Atomic Planning is a veteran-owned registered investment advisor. This content is for informational purposes only and is not personalized tax or investment advice.