How the IRS Taxes Retirement Income in 2026: What’s Taxable, What’s Not, and Planning Tips

Retirement planning starts with knowing how the IRS taxes different types of income. And 2026 brings updated brackets, thresholds, and numbers worth knowing before you start drawing down your savings.

If most of your retirement savings are in a 401(k) or IRA, understanding the tax rules isn't optional. It's the difference between a retirement that works and one that quietly costs you tens of thousands of dollars more than it should.

This guide covers:

How the 2026 standard deduction, the new senior deduction, and marginal tax brackets work (with real examples)

Which retirement income sources are taxable and how much

Which sources are completely tax-free

How Social Security taxation actually works (with the math)

How Medicare Income-Related Monthly Adjustment Amount (IRMAA) surcharges can affect your retirement costs

How state taxes can affect your retirement income

Practical tax planning strategies to reduce your lifetime tax bill

Let's start with the foundation: what actually gets taxed and at what rate.

The 2026 Standard Deduction

Before the tax brackets even come into play, most retirees reduce their taxable income by taking the standard deduction. In 2026 that's:

$16,100 for single filers

$32,200 for married couples filing jointly (Married Filing Jointly, or MFJ)

This means a married couple would need more than $32,200 in combined retirement income before they owe any federal income tax at all.

And if you're 65 or older, you get an additional deduction on top of that. For 2026 it's an extra $1,650 per person for married filers, or $2,050 for single filers. So a married couple where both spouses are 65 or older would have a combined standard deduction of $35,500 before a single dollar is taxed.

The New Enhanced Senior Deduction (Age 65+)

For 2026-2028, taxpayers age 65 and older can claim an additional deduction of up to $6,000 per eligible individual, regardless of whether they itemize or take the standard deduction. This is a below-the-line deduction, meaning it reduces your taxable income on top of whatever other deductions you already take.

A few important details:

It's per person, so a married couple where both spouses are 65 or older could potentially deduct up to $12,000 combined.

The deduction phases out based on income. For single filers, it begins phasing out at $75,000 and is fully phased out at $175,000. For married couples filing jointly, the phaseout runs from $150,000 to $250,000.

Because the phaseout ranges align closely with the income levels of many pre-retirees and early retirees, managing your taxable income in those years can directly affect whether you capture the full deduction, a partial deduction, or none at all.

Example: A married couple, both age 67, with $160,000 in taxable income would be $10,000 into the phaseout range, reducing their combined $12,000 senior deduction somewhat. But a couple who strategically draws from Roth accounts to bring taxable income down to $150,000 would capture the full $12,000 deduction. That's a meaningful difference, and exactly the kind of planning that pays off in retirement.

Note: Confirm the exact phaseout calculation method with a tax professional.

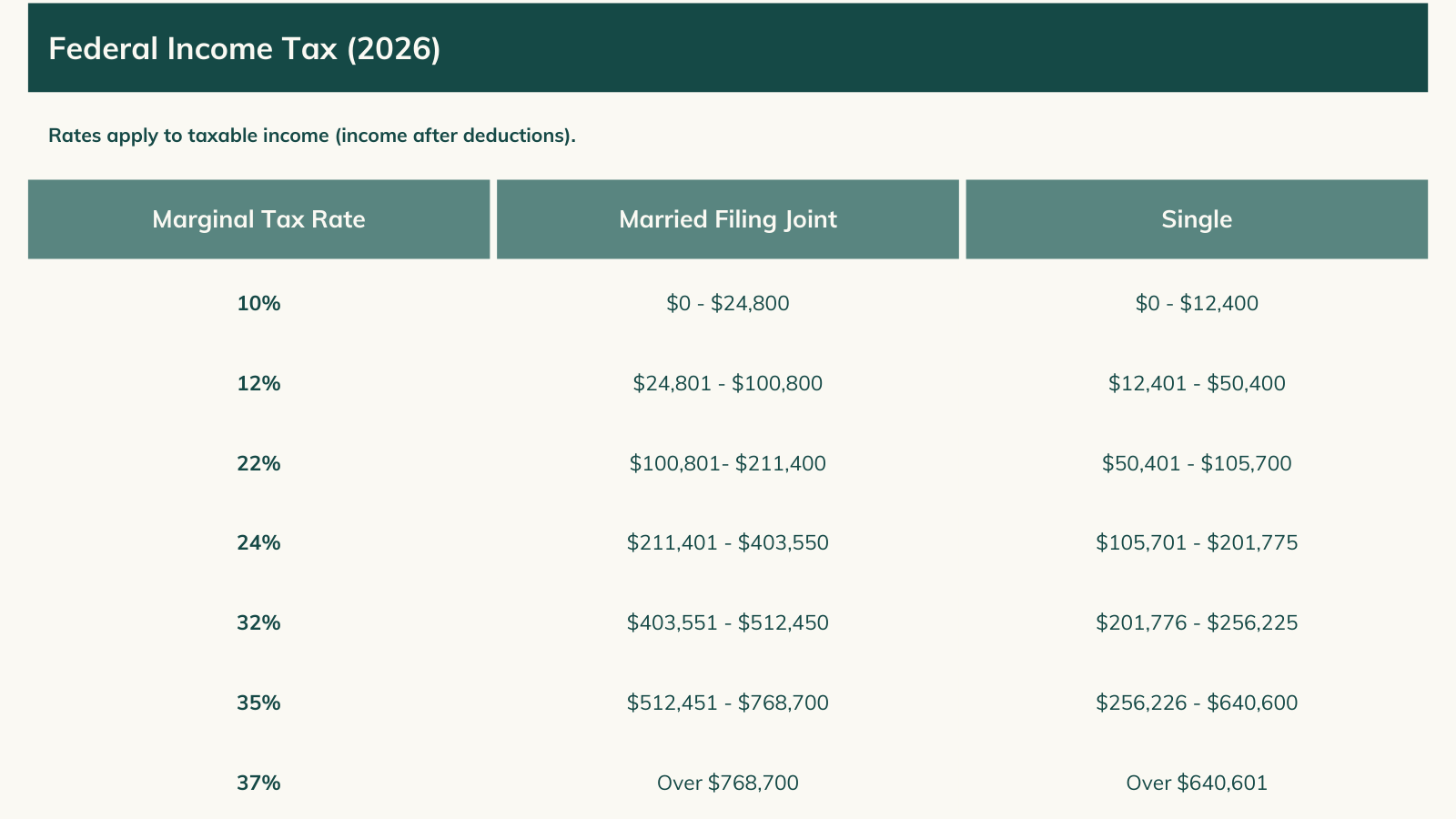

2026 Marginal Tax Rates Explained

A common misunderstanding is that moving into a higher tax bracket means all of your income gets taxed at the higher rate. That's not how it works. Marginal tax rates mean you're only taxed at higher rates on the portion of income that falls within each bracket, not your entire income.

Example: Let’s say you are single filer with $150,000 in taxable income in 2026.

1. Your first $12,400 is taxed at 10% = $1,240

2. Your next $38,000 is taxed at 12% = $4,560

3. Your next $55,300 is taxed at 22% = $12,166

4. Your next $44,300 is taxed at 24% = $10,632

Total federal tax: $28,598

Even though the highest rate you'd pay is 24%, only the income above $105,700 is taxed at that rate. The majority of your income is taxed at lower rates.

This matters a lot in retirement because you have much more control over your taxable income than you did while working. Strategic withdrawals, Roth conversions, and timing decisions can keep you in lower brackets year after year and help you capture deductions like the new senior deduction before they phase out.

Taxable Income Sources in Retirement

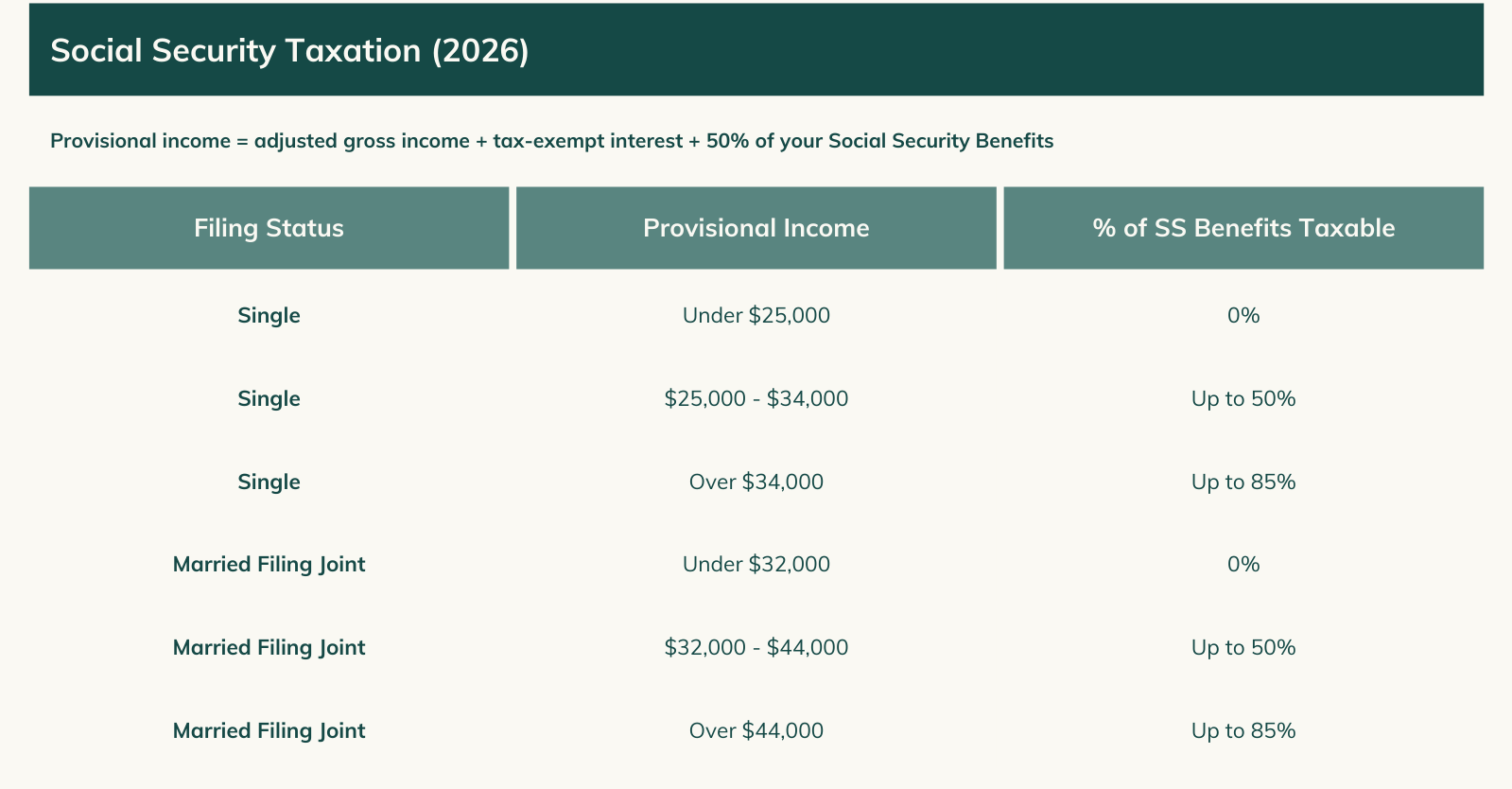

Social Security Benefits

Social Security is partially taxable for most retirees, but the calculation trips up a lot of people. Whether your benefits are taxed (and how much) depends on your "provisional income."

Provisional income = your adjusted gross income + tax-exempt interest + 50% of your Social Security benefits

Here's how the thresholds work for 2026:

Real example: Say you and your spouse receive $40,000/year in Social Security and take $50,000 from your 401(k). Your provisional income is $50,000 + $20,000 (half of SS) = $70,000. That's well above $44,000, so up to 85% of your Social Security (or $34,000) could be subject to federal income tax.

This is why how and when you withdraw from your retirement accounts can directly impact how much of your Social Security gets taxed. It's one of the most underestimated planning levers available to pre-retirees.

Traditional IRAs and 401(k)s

Distributions from traditional IRAs and 401(k)s are fully taxable as ordinary income, assuming your contributions were made pre-tax (which is true for the vast majority of people).

A few key rules to know:

Required Minimum Distributions (RMDs) begin at age 73 if you were born before 1960, or age 75 if born in 1960 or later. You can't leave the money in a traditional account indefinitely. The IRS requires you to start taking withdrawals, and those withdrawals are taxed as income.

Early withdrawals (before age 59½) are taxed as ordinary income and hit with a 10% penalty, with some exceptions.

Large RMDs can push you into higher tax brackets and trigger higher Medicare premiums (more on that below). This is why starting Roth conversions before RMDs kick in can be so valuable.

Pension Income

Pension payments are taxed as ordinary income in most cases. If you made after-tax contributions during your working years, a portion of each payment may be tax-free. The IRS uses what's called the "Simplified Method" to calculate this.

Investment Income

Interest income: Interest from savings accounts, CDs, and bonds held in taxable accounts is taxed as ordinary income.

Qualified dividends: Taxed at the more favorable long-term capital gains rates (0%, 15%, or 20%) rather than ordinary income rates.

Capital gains: If you sell an investment held for more than a year, the gain is taxed at long-term capital gains rates. Investments held for less than a year are taxed as ordinary income.

One important nuance: capital gains are "stacked" on top of your ordinary income when determining your rate. So if you have $60,000 in ordinary income and $20,000 in capital gains, the gains are taxed as if they were the top layer of your income.

Annuities

Annuities purchased with pre-tax funds (like rolling a 401(k) into an annuity) are fully taxable as ordinary income when distributed.

Annuities purchased with after-tax dollars have only the earnings portion taxed. Your original contributions come back to you tax-free.

Rental Income

Net rental income (after deducting expenses like mortgage interest, property taxes, maintenance, and depreciation) is taxed as ordinary income. Depreciation deductions can meaningfully reduce your taxable rental income, but be aware of depreciation recapture when you eventually sell the property.

Part-Time Work or Self-Employment

Wages and self-employment income in retirement are subject to ordinary income tax. Self-employment income is also subject to self-employment tax (Social Security and Medicare), though you can deduct half of that on your return.

Non-Taxable Income Sources

Roth IRAs and Roth 401(k)s

This is the gold standard of tax-free retirement income. Qualified withdrawals from Roth accounts (both contributions and earnings) are completely tax-free, as long as:

The account has been open for at least five years, and

You're age 59½ or older

Roth accounts also have no RMDs during your lifetime, giving you full control over when and how much you withdraw. This flexibility is one reason why Roth conversions before retirement can be so powerful for people with large traditional IRA or 401(k) balances.

Health Savings Accounts (HSAs)

HSAs are one of the most underused tools in retirement tax planning. Distributions used for qualified medical expenses are completely tax-free, not just tax-deferred. After age 65, you can withdraw HSA funds for any reason and pay only ordinary income tax with no penalty, making them function like a traditional IRA as a fallback.

If you're still working and eligible, maxing out your HSA contributions and letting them grow invested is a powerful strategy.

Municipal Bond Interest

Interest from municipal bonds is exempt from federal income tax. If the bonds are issued in your state of residence, they're typically exempt from state income tax too. The tradeoff is lower yields compared to taxable bonds, but for retirees in higher tax brackets, the after-tax return can be competitive.

Note: municipal bond interest is included in provisional income for Social Security taxation purposes, so large muni holdings can still indirectly affect your SS tax bill.

Life Insurance Death Benefits

Life insurance proceeds paid to a beneficiary are generally not subject to income tax. However, any interest earned on those proceeds after the insured's death is taxable.

Veterans Benefits

Disability payments, pensions, and education assistance from the VA are tax-exempt.

How State Taxes Affect Retirement Income

Federal taxes get most of the attention, but state taxes can take a significant additional bite depending on where you live, or nothing at all.

Here's a general breakdown:

States with no income tax (so retirement income isn't taxed at the state level): Florida, Texas, Nevada, Wyoming, South Dakota, Washington, Alaska, Tennessee, and New Hampshire.

States that fully exempt Social Security: Most states don't tax Social Security at all, including Kansas and Missouri, which is good news if you're in the Kansas City area (like me).

States that tax most retirement income: States like California and Minnesota treat most retirement income similarly to ordinary income, with few exemptions.

States with partial exemptions: Many states offer specific deductions or exemptions for pension income, military retirement, or retirement accounts up to a certain dollar amount.

If you're considering relocating in retirement, the state tax picture is worth modeling carefully. Moving from a high-tax state to a no-income-tax state can save a meaningful amount annually, but it needs to be weighed against cost of living, healthcare access, and proximity to family.

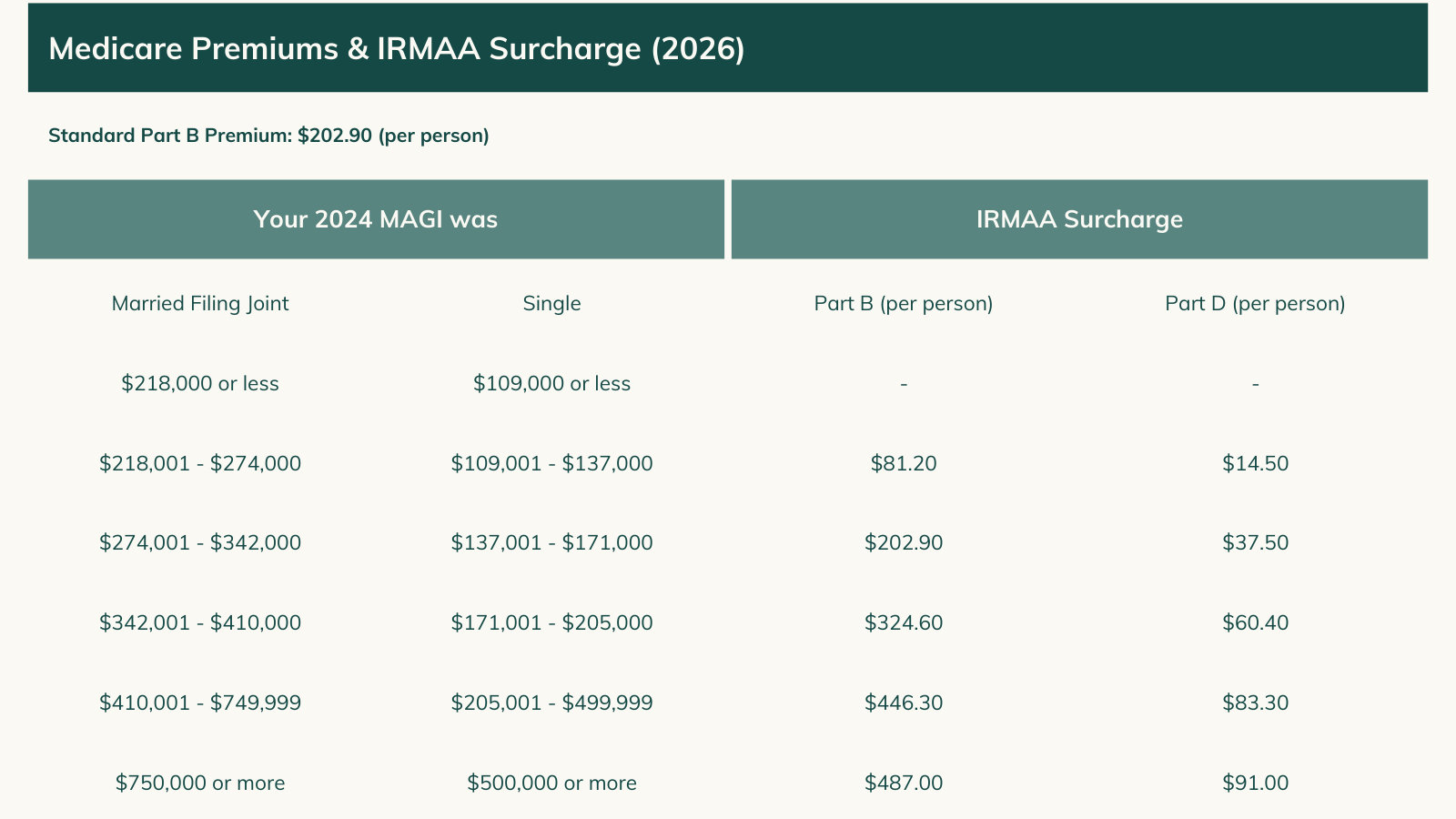

The Medicare IRMAA Trap

This one catches a lot of people off guard. Medicare Part B and Part D premiums aren't fixed. They're based on your income from two years prior. This is called the Income-Related Monthly Adjustment Amount, or IRMAA.

In 2026, if your modified adjusted gross income (MAGI) exceeds certain thresholds, you'll pay significantly higher Medicare premiums on top of the standard amount. For married couples filing jointly, the surcharges kick in above $218,000 in MAGI (based on 2024 income).

Why does this matter for planning? A large Roth conversion, an RMD spike, or the sale of a property in a single year can push you into a higher IRMAA bracket, costing you thousands in additional Medicare premiums two years later. This is exactly the kind of "tax landmine" that a proactive retirement plan is designed to help you avoid.

Practical Tax Planning Strategies

1. Do Roth Conversions Before RMDs Begin

If you're in your 50s or early 60s and not yet taking Social Security or RMDs, you may be in a lower tax bracket than you'll be in later retirement, especially once RMDs force large taxable distributions. Converting a portion of your traditional IRA to a Roth each year during this window can reduce your future RMDs, lower lifetime taxes, and leave your heirs with a better inheritance.

We've helped some clients project significant long-term tax savings by spreading out conversions strategically over several years.

2. Manage Your Provisional Income to Reduce SS Taxes

If you can keep your provisional income below the thresholds outlined above, you can reduce or eliminate the taxation of your Social Security benefits. This might mean drawing from Roth accounts in certain years instead of your traditional IRA, or timing capital gains realizations carefully.

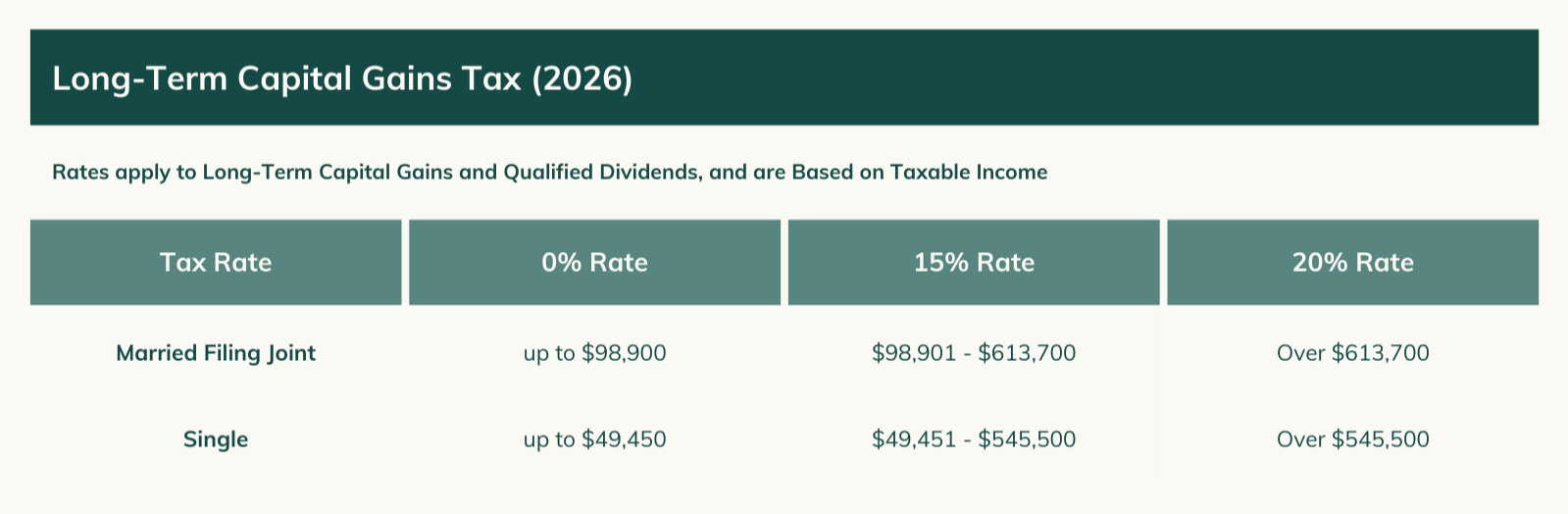

3. Use the 0% Capital Gains Bracket

In 2026, married couples filing jointly with taxable income below approximately $98,900 pay 0% federal tax on long-term capital gains. If you have appreciated investments in a taxable account, you may be able to strategically realize gains in low-income years (including early retirement before Social Security and RMDs kick in) and pay nothing in capital gains tax.

4. Coordinate Withdrawals Across Account Types

Most retirees have three "buckets": taxable accounts (brokerage), tax-deferred accounts (traditional IRA/401k), and tax-free accounts (Roth). Drawing from the right bucket at the right time, based on your income, brackets, and goals each year, is one of the most impactful things a good retirement plan can do for you.

5. Watch Your IRMAA Thresholds

Work backwards from the Medicare income thresholds when planning your annual income. In some cases, taking slightly less in a given year to stay below an IRMAA bracket is worth thousands in avoided premiums.

6. Consider Your State Tax Picture

If your state offers favorable treatment of retirement income, that's a meaningful factor in deciding which accounts to draw from and when. If you're in a high-tax state, Roth distributions (which are generally also state-tax-free) become even more valuable.Additional Questions About Retirement Taxes

Frequently Asked Questions

How does tax withholding work on retirement income? Taxes are often withheld from pensions, annuities, and IRA distributions automatically. You can adjust withholding by submitting a W-4P to the payer. Many retirees also make quarterly estimated tax payments to avoid underpayment penalties, especially if their income varies year to year.

How can I minimize taxes on Social Security? The most effective strategy is managing your provisional income. Drawing from Roth accounts instead of traditional accounts in certain years keeps your AGI lower, which can reduce how much of your Social Security is subject to tax. Delaying Social Security to increase your benefit amount can also reduce the total years you're subject to SS taxation.

What are the tax implications of selling my home in retirement? Homeowners can exclude up to $250,000 of capital gains ($500,000 for married couples) from the sale of a primary residence, provided you've lived in the home for at least two of the past five years. Gains above the exclusion are subject to capital gains tax.

What if I move abroad in retirement? U.S. citizens are required to report and pay taxes on worldwide income regardless of where they live. Some countries have tax treaties with the U.S. that can reduce double taxation, and the Foreign Earned Income Exclusion may apply in certain situations. This is a complex area that warrants professional guidance.

Do I need to file a tax return in retirement? It depends on your income level and sources. If your only income is Social Security below the provisional income thresholds, you may not need to file. But most retirees with IRA/401(k) distributions, pension income, or investment income will need to file annually.

In Closing

Understanding how retirement income is taxed in 2026 is the first step. Knowing what to do about it is where the real value lies. The decisions you make in the years leading up to retirement about Roth conversions, Social Security timing, withdrawal sequencing, and deduction planning can have a six-figure impact on your lifetime tax bill.

If you have $1 million or more in a 401(k) or IRA and want to understand what a personalized tax strategy could save you, we'd be glad to show you.

To your Atomic Retirement,

Ryan Kilkenny

P.S. If you have a question or would like help planning for retirement, you can schedule an appointment here.

Atomic Planning is a veteran-owned registered investment advisor. This content is for informational purposes only and is not personalized tax or investment advice.