Key Money Moves in Your 50s, 60s, and Beyond: A Financial Milestone Guide for 2026

The years between your 50th birthday and the start of Required Minimum Distributions (RMDs) are the most financially consequential stretch of your life. The decisions you make during this window, about saving, taxes, Social Security, Medicare, and retirement income, can mean the difference between a retirement that works and one that runs short.

Most people treat these years as a waiting room. The smart ones treat them as a planning opportunity.

This guide walks through every major financial milestone from age 50 to 75, with real context for what each one means and what you should actually do about it.

Age 50: Catch-Up Contributions Begin

This is one of the most valuable milestones in the tax code and one of the most underused.

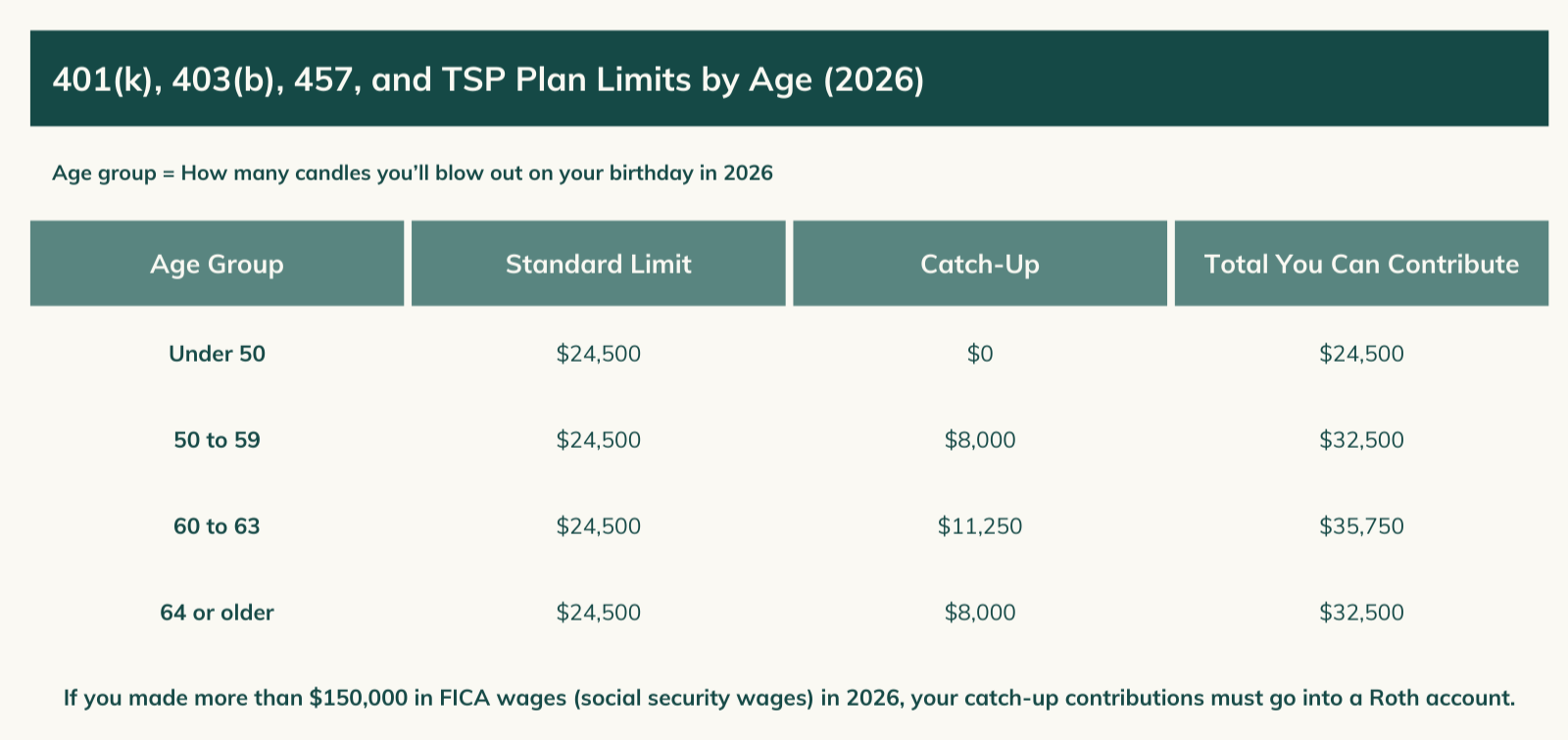

Once you turn 50, the Internal Revenue Service (IRS) allows you to make catch-up contributions to your retirement accounts on top of the standard annual limits. In 2026 that means:

401(k), 403(b), and 457 plans: An extra $8,000 per year on top of the $24,500 standard limit, for a total of $32,500

Individual Retirement Accounts (IRAs): An extra $1,100 per year on top of the $7,500 standard limit, for a total of $8,600

If you and your spouse are both 50 or older and both have access to workplace retirement plans, you could be sheltering up to $65,000 per year from taxes in those accounts alone. Over the 10-15 years before retirement, that additional savings compounds significantly.

What to do: Log into your 401(k) portal and confirm your contribution rate reflects the higher limit. Many people never update this and leave thousands of dollars of tax-advantaged savings on the table every year.

Also at age 50: Disabled widows and widowers become eligible for Social Security survivor benefits at a reduced rate.

Age 55: The Rule of 55 and HSA Catch-Up

The Rule of 55 is a little-known exception to the 10% early withdrawal penalty on retirement accounts. If you leave your job (voluntarily or otherwise) in the calendar year you turn 55 or later, you can take penalty-free withdrawals from that employer's 401(k) or 403(b) plan, without waiting until age 59½.

This matters most for people who retire early or are laid off in their mid-50s and need income before the normal penalty-free window opens. A few important caveats:

The rule applies only to the plan at the employer you're leaving, not to IRAs or old 401(k)s at former employers

You still owe ordinary income tax on withdrawals. The rule only eliminates the 10% penalty

Rolling the money to an IRA before using it forfeits the Rule of 55 benefit

Health Savings Account (HSA) catch-up: At 55, you can also contribute an extra $1,000 per year to your HSA on top of the standard limit. In 2026 the standard limits are $4,400 for individual coverage and $8,750 for family coverage, so the catch-up brings those to $5,400 and $9,750 respectively. If both spouses are 55 or older and each has their own HSA, each can make the catch-up contribution.

HSAs are one of the best savings vehicles available to pre-retirees. Contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free. It is a triple tax advantage you won't find anywhere else. If you can afford to pay medical expenses out of pocket now and let your HSA grow invested, the long-term value is substantial.

Age 59½: The Penalty-Free Withdrawal Window Opens

At 59½ you can withdraw money from any IRA or 401(k) without the 10% early withdrawal penalty. This is a meaningful milestone for two reasons.

First, it gives you flexibility. If you retire before 62 and don't have enough in taxable accounts or Roth accounts to cover expenses, you can now draw from traditional retirement accounts without penalty. You'll still owe income tax on those withdrawals, but the 10% penalty is gone.

Second, and more importantly for planning purposes, this is when your Roth conversion window opens. If you're still working (or recently retired) and your income is temporarily lower than it will be once Required Minimum Distributions (RMDs) and Social Security kick in, these years are often the best opportunity to convert traditional IRA or 401(k) money to Roth at relatively low tax rates.

For a full breakdown of why this window matters and how to use it, see our post on Roth conversion strategy for pre-retirees.

Age 60: Social Security Survivor Benefits

If you are a widow or widower, you become eligible for Social Security survivor benefits at age 60 (or 50 if you are disabled). Claiming at 60 means a reduced benefit, but it can be a valuable source of income if you need it.

One important planning note: if you're eligible for both survivor benefits and your own retirement benefit, you don't have to claim both at the same time. You can claim one while letting the other grow. For example, claiming the survivor benefit at 60 while letting your own retirement benefit grow to its maximum at age 70 can significantly increase your lifetime total, or vice versa depending on the amounts. This is a decision worth modeling carefully before you claim anything.

Ages 60-63: The Super Catch-Up Contribution

This is one of the most significant retirement savings provisions introduced in recent years, and most people in this age group have no idea it exists.

Under the SECURE 2.0 Act, employees ages 60, 61, 62, and 63 are eligible to make a super catch-up contribution to their employer-sponsored retirement plan (401(k), 403(b), or 457) in place of the standard age-50+ catch-up. In 2026 the super catch-up limit is $11,250 on top of the $24,500 standard limit, for a total of $35,750.

To put that in context:

A few important details:

The super catch-up is only available through employer plans (401(k), 403(b), 457). It does not apply to IRAs.

It applies to the calendar years in which you are ages 60, 61, 62, or 63. Once you turn 64, you revert to the standard age-50+ catch-up of $8,000.

Turning 64 this year? You are no longer eligible for the super catch-up, but you are still fully eligible for the regular age-50+ catch-up of $8,000. Your total annual limit is $32,500, not $35,750.

If your plan doesn't yet support the super catch-up, check with your HR department or plan administrator.

High earners take note: If you earned more than $150,000 in FICA wages (Social Security wages) in 2026, your catch-up contributions must go into a Roth account rather than a pre-tax account. This applies to all catch-up contributions, not just the super catch-up. Check with your plan administrator to confirm how your plan handles this requirement.

If you are in this four-year window and not taking advantage of it, you are leaving one of the most valuable savings opportunities in the tax code unused. For a married couple where both spouses are between 60 and 63 and both have access to workplace plans, the combined super catch-up capacity is $22,500 per year on top of regular contributions.

What to do: Contact your HR department or log into your 401(k) portal and confirm your contribution election reflects the $35,750 limit, not the standard $32,500. You may need to actively elect the higher amount.

Age 62: Social Security Retirement Benefits

Social Security: Age 62 is the earliest you can claim Social Security retirement benefits, but doing so permanently reduces your monthly benefit by up to 30% compared to your Full Retirement Age (FRA) amount. For people born in 1960 or later, Full Retirement Age is 67.

Claiming at 62 can make sense in certain situations: poor health, a surviving spouse who will receive your benefit, or a genuine need for income. But for most people with $1M+ in retirement savings, the math typically favors delaying. Every year you wait past 62 increases your benefit, and waiting from 67 to 70 earns you an additional 8% per year in guaranteed, permanent increases.

For a full breakdown of the claiming decision including the breakeven analysis and spousal strategy, see our Social Security guide.

Age 63: Start Planning for Medicare

Most people know Medicare begins at 65, but the planning needs to start at 63, specifically around Income-Related Monthly Adjustment Amount (IRMAA) surcharges.

Medicare Part B and Part D premiums are based on your income from two years prior. That means your 2026 income determines your 2028 Medicare premiums. If you have a high-income year at 63 or 64 due to a large Roth conversion, a bonus, or selling a property, it can trigger higher Medicare premiums two years later.

This isn't a reason to avoid Roth conversions, but it is a reason to model the impact before executing them. Sometimes spreading a large conversion over two years instead of one can save thousands in avoided IRMAA surcharges.

Age 64 and 9 Months: Medicare Initial Enrollment Period Begins

Your Medicare Initial Enrollment Period (IEP) is a 7-month window that starts 3 months before the month you turn 65, includes your birth month, and ends 3 months after. Missing this window without qualifying for a Special Enrollment Period can result in permanent late enrollment penalties on your Part B premiums.

If you're still covered by an employer health plan at 65, you may be able to delay Medicare enrollment without penalty, but the rules are specific and the consequences of getting it wrong are expensive. Get clear on your situation before your IEP opens.

Age 65: Medicare Eligibility and HSA Contribution Deadline

At 65 you become eligible for Medicare. If you're receiving Social Security at this point, you'll be enrolled in Medicare Part A (hospital insurance) automatically. Part B (medical insurance) requires active enrollment.

One important HSA rule: you must stop contributing to your HSA once you enroll in Medicare, including Part A. If you plan to delay Medicare and keep contributing to your HSA past 65, make sure you understand exactly when your Medicare coverage begins. It can be retroactive in some cases, which can create a tax problem if you contributed during a period you were technically covered.

After 65, you can withdraw HSA funds for any purpose without the 20% penalty (you'll owe ordinary income tax on non-medical withdrawals, just like a traditional IRA). For qualified medical expenses, withdrawals remain completely tax-free at any age.

Age 67: Full Retirement Age for Most People

For anyone born in 1960 or later, age 67 is your Full Retirement Age (FRA) for Social Security. This is the age at which you receive your full Primary Insurance Amount (PIA) with no reductions. If you claim before 67, your benefit is permanently reduced. If you claim after 67, your benefit grows by 8% per year until age 70.

This is also the age at which the Social Security earnings test disappears entirely. Before FRA, earning above certain thresholds while receiving Social Security results in withheld benefits. At FRA and beyond, you can earn any amount with no impact on your Social Security benefit.

If you were born between 1955 and 1959, your Full Retirement Age is between 66 and 67, specifically:

Born 1955: FRA is 66 and 2 months

Born 1956: FRA is 66 and 4 months

Born 1957: FRA is 66 and 6 months

Born 1958: FRA is 66 and 8 months

Born 1959: FRA is 66 and 10 months

Age 70: Maximum Social Security Benefit

At 70, your Social Security benefit stops growing. If you haven't claimed yet, there is no further financial benefit to waiting. This is the age to claim if you've been delaying for the maximum benefit.

For someone with a Full Retirement Age benefit of $2,800/month, the age 70 benefit would be approximately $3,696/month, a 32% increase over the FRA amount, and a permanent, inflation-adjusted income stream for life.

Use our Social Security Lifetime Benefit Calculator to see what your own numbers look like across different claiming ages.

Age 70½: Qualified Charitable Distributions Become Available

At 70½ you can make Qualified Charitable Distributions (QCDs) directly from your IRA to a qualifying charity. In 2026, the annual QCD limit is $111,000 per person ($222,000 for a married couple if both have IRAs).

QCDs are one of the most tax-efficient ways to give to charity in retirement. The distribution counts toward your RMD for the year but is excluded from your taxable income entirely, meaning it doesn't increase your Adjusted Gross Income (AGI), doesn't affect Social Security taxation thresholds, and doesn't push you into higher IRMAA brackets. For charitably inclined retirees, this is significantly better than taking the RMD, paying income tax on it, and then donating after-tax dollars.

Age 73: Required Minimum Distributions Begin (Born Before 1960)

If you were born before 1960, the IRS requires you to start taking Required Minimum Distributions (RMDs) from your traditional IRAs and 401(k)s at age 73. These withdrawals are calculated each year based on your account balance and your life expectancy factor from the IRS Uniform Lifetime Table.

RMDs are fully taxable as ordinary income. For people with large pre-tax retirement account balances, RMDs can be substantial, large enough to push you into higher tax brackets, increase the taxable portion of your Social Security, and trigger higher Medicare IRMAA surcharges.

This is precisely why the years between 59½ and 73 are so valuable for Roth conversions. Every dollar you convert before RMDs begin is a dollar that won't be forced out of your account at the IRS's schedule. A well-executed conversion strategy can significantly reduce your RMD burden and save a substantial amount in lifetime taxes.

Missing an RMD carries a steep penalty: 25% of the amount that should have been withdrawn (reduced to 10% if corrected quickly).

Age 75: Required Minimum Distributions Begin (Born in 1960 or Later)

If you were born in 1960 or later, your RMD start date is pushed to age 75 under the SECURE 2.0 Act. This gives you two additional years of Roth conversion opportunity and tax-deferred growth compared to those born before 1960.

The same planning principles apply: use the years before RMDs begin to reduce the pre-tax balance through strategic Roth conversions, taking advantage of lower tax brackets while you still control your taxable income.

The Thread That Runs Through All of It

Looking across these milestones, a clear theme emerges: the years between 50 and the start of RMDs are a planning window that most people never fully use.

Catch-up contributions, Roth conversions, Social Security timing, Medicare coordination, HSA maximization, and QCDs all interact with each other. The decisions you make in these years compound in both directions. Done well, they can reduce your lifetime tax bill by six figures and give you significantly more flexibility and security in retirement. Done poorly, or not at all, they can lock in a higher tax burden for decades.

If you have $1 million or more in pre-tax retirement accounts and want to understand what a coordinated plan could save you, we'd be glad to show you.

To your Atomic Retirement,

Ryan Kilkenny

P.S. If you have a question or would like help planning for retirement, you can schedule an appointment here.

Atomic Planning is a veteran-owned registered investment advisor. This content is for informational purposes only and is not personalized tax or investment advice.